Notes from the Front Row: The Sharpest Edge Is a K

Day One at NYU IHIF 2026, where America’s largest service export met the lowest consumer sentiment in 75 years.

The opening montage played like a highlight reel: “This is where capital meets execution.” “Opportunity favors investors who sharpen their edge.” “Drive alpha and unlock value to lead the next cycle.” The music hit right. The energy in the Marriott Marquis ballroom was high. Two thousand two hundred delegates. Seven hundred equity investors. Alexi Khajavi called it the strongest investor attendance cohort in forty-eight years of this conference.

Then, one minute later, Alexi said something quieter: “Capital is not flowing broadly.”

That sentence was the first gear of the day. Because everything that followed, across four sessions and roughly eight hours, lived inside the tension between those two ideas. Smart capital is here. And it is pointed at a very specific part of the market.

The K

Anthony Scaramucci, fondly called the Mooch, named it twenty minutes into his fireside chat. “We are operating in a K, ladies and gentlemen.”

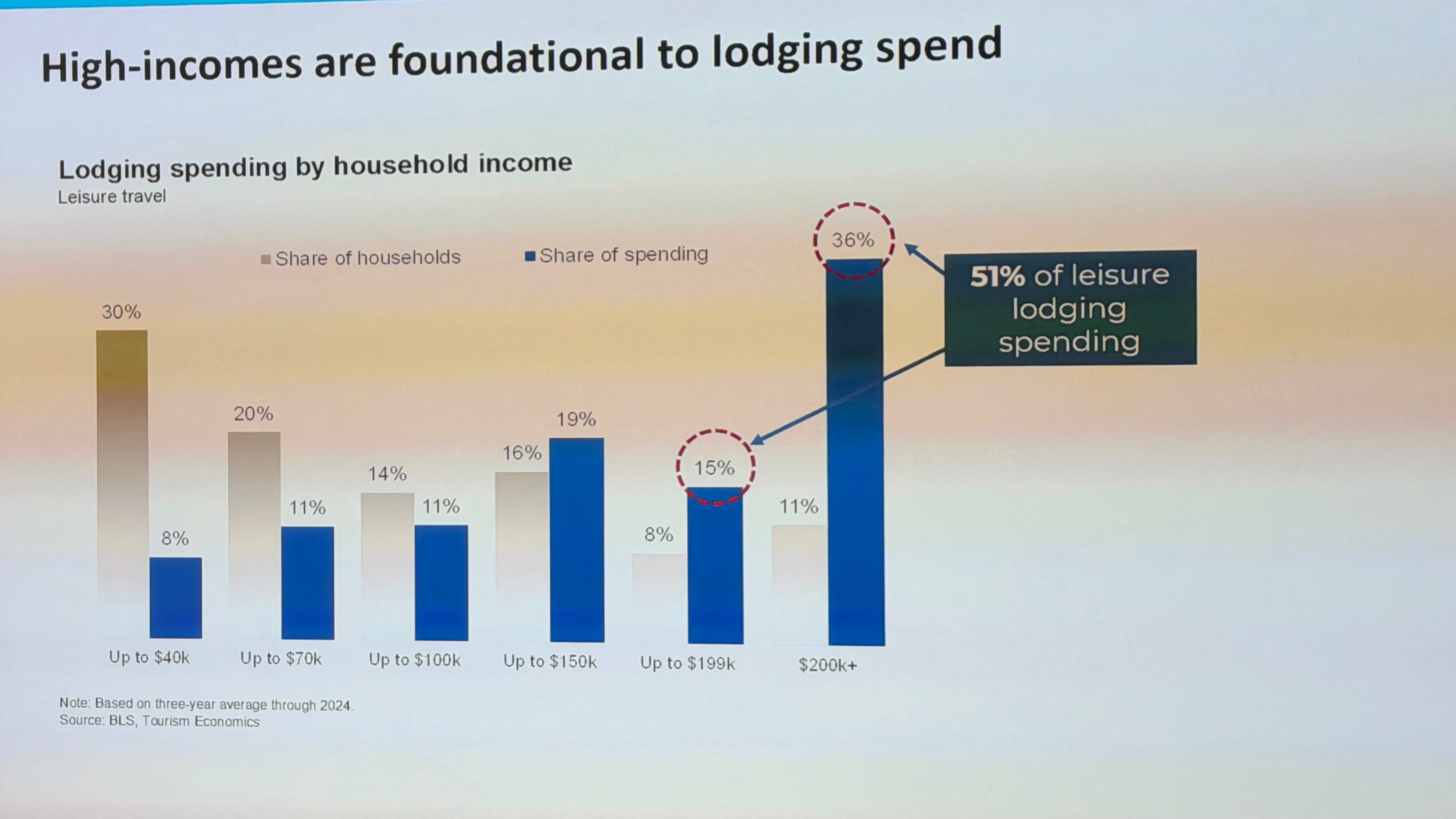

The data backed him up. The economist on the main stage showed the split: upscale and upper midscale demand is up 9.3% relative to 2019. Midscale and economy? Still down 8%. Consumer sentiment hit the lowest reading in 75 years in April. But spending from the top hasn’t slowed. Fifty-one percent of leisure travel spending in lodging comes from households making $150,000 or more. That’s 19% of American households driving more than half the revenue.

That is bananas to me.

The top 1% has seen nearly a doubling of net worth as a share of household income. Hotels with an ADR over $1,000 have tripled since 2019. Wealth has not tripled since 2019. (Barbara Muckermann dropped that line on the luxury panel, and it landed.)

Meanwhile, international visitation to the U.S. is sliding. Overseas travel is down 4.3% through April, on top of a 2.5% decline last year. Canadian travel fell 25% in 2025 and another 11% in the first four months of 2026. RevPAR is forecast to grow 2.8% this year, but when FF&E costs are up 25% and labor is up 40 to 50% since 2019, you start to wonder how much of that growth is real.

Scaramucci put it plainly: “The median income in the United States right now is eighty-three thousand dollars. The median house price is four hundred and thirty-two thousand. You can’t buy the house.” And then, because he’s Scaramucci: “Knicks in five.”

(He also said the Constitution hasn’t been meaningfully amended in 59 years, that the country is “very, very fixable,” and that he got fired from the White House in eleven days, not ten. Don’t hurt his feelings.)

What Do Guests Actually Need?

The luxury panels asked the right question. Jack Ezon, who doesn’t need a microphone to fill a room, said it best: “Ninety-nine percent of what we sell, people don’t need. The only thing they really need is to feel loved.”

Barbara Muckermann from Kempinski pushed back: people want to leave in a better state than they came in. But then she said the quieter thing: “If I cannot explain why you should come to our hotel versus another, I’m just selling a bed. And then Airbnb is the clear winner.”

That’s the tension at the top of the K. The capital is flowing to luxury. The branded residential pipeline has 1,077 projects globally (the U.S. accounts for 23% of that market). But the proliferation of luxury brands is outpacing the consumer’s ability to tell them apart. Tiffany Cooper from Mandarin Oriental asked the obvious follow-up: is there a bubble?

What is separating the winners? Not marble. Tiffany said luxury has moved away from opulence and excess toward “approachability of service, connecting with people on a very human level.” Jake Pinsof from Marriott talked about dedicated directors of culture and entertainment at W and Edition properties. Leanne Harwood from IHG made the point I keep coming back to: programming is everything. “If we don’t bring the brand to life with active programming, we’re not going to get the rate, and then we don’t get the revenue, and then it just becomes a whopping great big spiral down to the bottom.”

The metric is shifting too. RevPAR used to be the only number that mattered. In luxury and lifestyle, TRevPAR (total revenue per available room) is becoming the benchmark, because so much of the revenue lives in food and beverage, wellness, experiences, and programming. Not just the room.

But I’ll be honest: I’m not 100% sold on this from a valuation perspective. From my experience, RevPAR still outweighs TRevPAR. I’d like the latter to be true, especially in complicated experiential properties. But I think the former still rules the roost. I’d love to be wrong here.

Sweating the Asset

I really enjoyed “Sweating the Asset,” moderated by Esther Hertzfeld. Sarah Gulla from Pebblebrook, Paul McElroy from Highgate, and Jess Conroy from ROH.

Paul said something that sounds obvious until you sit with it: the most impactful investment in a guestroom right now might be better blackout drapes, better soundproofing, and a better mattress. Not necessarily a flashy lobby bar. Not a new spa. A good night’s sleep. “When they leave, they don’t feel like they need a vacation from their vacation. They actually feel restored.”

I’ve never heard an asset manager talk about blackout drapes before. Thank you, Paul. Sometimes the simplest answer is the best answer.

Sarah made the FF&E point that anyone in the casegoods business should hear: “If you buy good enough quality case goods, you can refurbish them, you can change the toppers, and they can last way longer than a typical lifecycle.” Pebblebrook is challenging brand PIPs on exactly this basis: is a renovation driven by condition, by guest demand, or just by the calendar? That’s a conversation that saves owners real money, and it’s one BERMANFALK has with owners every day.

Jess nailed the operational side: “If you have old piping and you put pristine water through it, the water gets mucky.” Revenue generation is great. But if the financial infrastructure underneath the hotel can’t move the dollars efficiently, the top line never hits the bottom line.

And aside from the Mooch’s Knicks fever dream, Jeff Stulmaker from KHP Capital Partners made the best statement of the day. When asked how he gets LPs to invest in private hotels versus public REITs, his answer was direct: “We do a public market equivalent analysis. How does an investment with us work versus the public markets over the same duration? We crush them every time.” (I like that line.)

Hooray for some recent examples: One Hotel Seattle, Hotel Viking, The Jay in San Francisco, and a couple more in development that I’ll keep on the down low.

The Edge

“Sharpening the Edge” is the conference theme this year. After Day One, I think the edge is simpler than people are making it.

The edge is knowing which side of the K you’re building for. The edge is active programming, not just beautiful product. The edge is a good night’s sleep (seriously). The edge is case goods built well enough to refinish instead of replace. The edge is asking whether your guest needs to be transformed, or just needs to feel loved.

I’m curious to find somebody who’s solved for the lower part of the K, because I heard the phrase “pitchforks and torches” more than three times throughout the day. Gilded ages can be fun, but the hangovers are not: hello, Marie Antoinette. Hello, Teddy Roosevelt and the trust busters. I heard “let them eat cake” more than twice across the sessions. That should make us all pause.

And for the people who actually deliver the guest experience (the designers, the purchasing agents, the manufacturers), the edge is execution speed. When the renovation window opens, it opens once. A manufacturer set up to deliver casegoods, seating, and a model room fast enough to keep pace with the construction calendar is the edge that shows up in the guest review, not the earnings call.

More tomorrow from Day Two.

Sorry I missed saying hello today :-) This is the part people should be paying attention to - capital is here, but it isn’t flowing broadly.

The 19% of households driving 51% of leisure lodging spend feels like more than a luxury trend.... it feels like a warning label. Hospitality has always been aspirational, but if the entire growth story depends on the top of the K continuing to spend, we should probably be asking harder questions about what happens to the rest of the market.

I loved the point about the edge being simpler than we make it: sleep, programming, differentiation, execution. But I’m especially interested in your question about who is actually solving for the lower part of the K.

Because that may be the bigger long-term opportunity: not just building more expensive experiences for fewer people, but figuring out how hospitality can still create restoration, belonging, and value for the guests who are increasingly being priced out of the story

Outstanding summary- and interesting numbers around attendance and by whom… Very curious to see what Day 2 reveals. I’m also curious about the mixed messages regarding the World Cup bump in general…